Personal finance is a critical aspect of our daily lives, yet many people overlook its importance. It encompasses everything related to managing your money, including budgeting, saving, investing, and planning for the future. Mastering personal finance can provide financial security, reduce stress, and help you achieve your financial goals. This article will guide you through the basics of personal finance and offer practical tips for managing your money effectively.

Importance of Mastering Personal Finance

Understanding and managing personal finance is essential for several reasons. First, it helps you make informed decisions about your money, ensuring you can cover your expenses and save for future needs. Second, it reduces financial stress, providing peace of mind and stability. Finally, mastering personal finance empowers you to achieve your financial goals, whether buying a home, starting a business, or retiring comfortably.

1. Setting Financial Goals

Setting clear financial goals is the first step toward financial success. Goals give you direction and a sense of purpose, helping you stay focused and motivated.

SMART Goals

To be effective, your financial goals should be SMART: Specific, Measurable, Achievable, Relevant, and Time-bound. For example, instead of saying, “I want to save money,” a SMART goal would be, “I want to save $5,000 for a down payment on a car within the next 12 months.”

Short-term vs. Long-term Goals

It’s essential to differentiate between short-term and long-term goals. Short-term goals are those you aim to achieve within a year, such as paying off credit card debt or saving for a vacation. Long-term goals take several years to achieve, such as buying a house or planning for retirement. Balancing both types of goals ensures you are making progress in the present while preparing for the future.

2. What is Budgeting?

Budgeting is the process of creating a plan for how you will spend your money. This plan helps you ensure that you have enough money to cover your essential expenses and allocate funds towards your financial goals. A budget can prevent overspending, reduce debt, and increase savings.

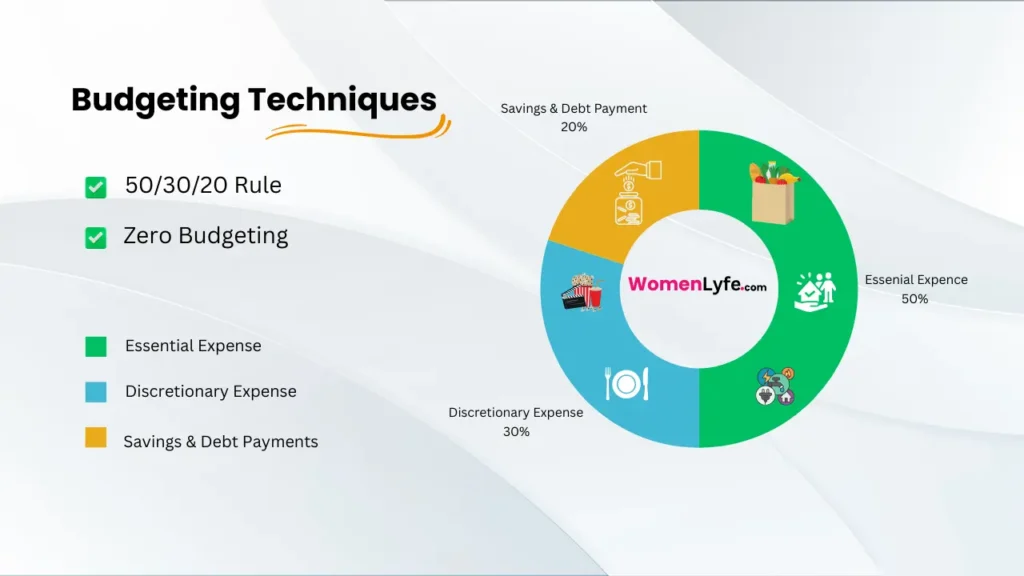

Budgeting Techniques

There are various budgeting techniques you can use to manage your finances effectively. Here are two popular methods:

50/30/20 Rule

The 50/30/20 rule is a simple budgeting framework. It suggests that you allocate 50% of your income to essential expenses (housing, utilities, groceries), 30% to discretionary expenses (entertainment, dining out), and 20% to savings and debt repayment. This rule provides a balanced approach to managing your finances without being overly restrictive.

Zero-based Budgeting

Zero-based budgeting involves allocating every dollar of your income to specific expenses, savings, or debt repayment, ensuring that your income minus expenses equals zero. This method requires detailed tracking of expenses but can be highly effective in maximizing savings and reducing wasteful spending.

3. Managing Debt Wisely

Debt management is crucial for financial health. Mismanaged debt can lead to high-interest payments and financial stress. Here are two strategies for managing debt wisely:

Paying Off High-Interest Debt First

Focusing on paying off high-interest debt first can save you money in the long run. High-interest debts, such as credit card balances, can accumulate quickly, so prioritizing these payments can reduce the overall interest you pay.

Consolidating Debt

Debt consolidation involves combining multiple debts into a single loan with a lower interest rate. This approach can simplify payments and potentially reduce the interest you pay, making it easier to manage your debt.

4. Building an Emergency Fund

An emergency fund is a savings buffer that covers unexpected expenses, such as medical bills or car repairs.

Importance of Emergency Funds

Having an emergency fund is crucial because it provides financial security and peace of mind. It ensures that you can handle unexpected expenses without going into debt or derailing your financial goals. Aim to save at least three to six months’ worth of living expenses in your emergency fund.

5. Investing for the Future

Investing is essential for building wealth and securing your financial future. It involves putting your money into assets that can grow over time, such as stocks, bonds, or real estate.

Basics of Investing

The basics of investing include understanding risk and return, setting investment goals, and choosing the right investment vehicles. Start by educating yourself on the different types of investments and how they work.

Types of Investment Accounts

There are various types of investment accounts, each with its benefits. Common options include individual retirement accounts (IRAs), 401(k) plans, and brokerage accounts. Each account type has different tax implications and rules, so it’s essential to choose the right one based on your goals and circumstances.

Retirement Accounts

Retirement accounts, such as IRAs and 401(k)s, offer tax advantages that can help you save more for retirement. Contributing regularly to these accounts can ensure you have enough money to maintain your lifestyle in retirement.

Also read

6. Diversification

Diversification involves spreading your investments across different asset classes to reduce risk. By not putting all your eggs in one basket, you can protect your portfolio from significant losses if one investment performs poorly.

7. Tracking Expenses

Tracking your expenses is a vital part of managing your finances. It helps you understand where your money is going and identify areas where you can cut back.

Benefits of Expense Tracking

The benefits of tracking expenses include better financial awareness, improved budgeting, and increased savings. By knowing your spending habits, you can make more informed decisions and stay on track with your financial goals.

Expense Tracking Apps

There are many expense tracking apps available that can simplify the process. These apps automatically categorize your spending, provide insights, and help you stay within your budget. Popular options include Mint, YNAB (You Need A Budget), and PocketGuard.

Manual Tracking Methods

If you prefer a more hands-on approach, you can track your expenses manually using a spreadsheet or a notebook. This method requires more effort but can provide a deeper understanding of your spending habits.

8. Avoiding Impulse Purchases

Impulse purchases can derail your budget and hinder your financial goals. Here are some tips to avoid them:

Impact on Finances

Impulse purchases can lead to unnecessary spending and debt. They often result from emotional triggers and can create financial strain if not managed properly.

Creating a Waiting Period

One effective strategy to avoid impulse buying is to create a waiting period before making a purchase. For example, wait 24 hours before buying non-essential items. This period allows you to evaluate whether the purchase is necessary and aligns with your financial goals.

9. Differentiating Between Needs and Wants

Understanding the difference between needs and wants is crucial for financial discipline. Needs are essential for survival and well-being, such as food and shelter. Wants are non-essential items that can enhance your lifestyle but are not necessary. Prioritizing needs over wants can help you make better financial decisions.

10. Continuous Learning and Improvement in Financial Literacy

Financial literacy is an ongoing journey. Staying informed and continuously learning about personal finance can help you make better financial decisions.

Reading Books and Articles

Reading books and articles on personal finance can expand your knowledge and provide valuable insights. Some recommended books include “Rich Dad Poor Dad” by Robert Kiyosaki and “The Total Money Makeover” by Dave Ramsey.

Attending Workshops and Seminars

Attending workshops and seminars on personal finance can provide practical advice and networking opportunities. Look for local events or online webinars that cover topics relevant to your financial goals.

Conclusion

Mastering personal finance is a lifelong journey that requires dedication and continuous learning. By setting financial goals, budgeting effectively, managing debt wisely, building an emergency fund, investing for the future, tracking expenses, avoiding impulse purchases, and staying informed, you can achieve financial security and peace of mind. Remember, the key to financial success is making informed decisions and staying committed to your financial goals.

Frequently Asked Questions (FAQs) on Personal Finance

1. What is personal finance?

Personal finance refers to the management of an individual’s financial activities, including income generation, budgeting, saving, investing, and planning for the future. It encompasses all financial decisions and activities of an individual or household, such as managing expenses, handling debt, and planning for retirement.

2. Why is budgeting important?

Budgeting is crucial because it helps you control your spending, save more money, and stay out of debt. By creating a budget, you can track your income and expenses, ensuring that you allocate your resources effectively to meet your financial goals and cover essential expenses.

3. How can I set effective financial goals?

To set effective financial goals, use the SMART criteria:

Specific: Clearly define what you want to achieve.

Measurable: Quantify your goal to track progress.

Achievable: Ensure your goal is realistic and attainable.

Relevant: Align your goal with your financial needs and values.

Time-bound: Set a deadline for achieving your goal.

Example: “I want to save $5,000 for a vacation in the next 12 months.”

4. What is the 50/30/20 rule in budgeting?

The 50/30/20 rule is a simple budgeting technique that divides your after-tax income into three categories:

50% for essential expenses (housing, utilities, groceries).

30% for discretionary expenses (entertainment, dining out).

20% for savings and debt repayment. This method helps you balance spending on necessities, lifestyle choices, and future financial security.

5. How can I manage debt effectively?

To manage debt effectively:

Pay off high-interest debt first: Focus on paying down debts with the highest interest rates to save money on interest.

Consolidate debt: Combine multiple debts into a single loan with a lower interest rate to simplify payments and potentially reduce interest costs.

Create a debt repayment plan: Set a timeline and specific amounts to pay off your debts consistently.

6. Why is an emergency fund important?

An emergency fund is essential because it provides a financial safety net for unexpected expenses, such as medical bills, car repairs, or job loss. Having three to six months’ worth of living expenses saved in an easily accessible account can prevent financial stress and keep you from going into debt during emergencies.

7. How should I start investing for the future?

To start investing:

Educate yourself: Learn the basics of investing, including different asset classes (stocks, bonds, real estate) and their risks and returns.

Set investment goals: Determine what you are investing for (e.g., retirement, buying a house) and your time horizon.

Choose the right accounts: Consider tax-advantaged accounts like IRAs and 401(k)s for retirement savings, and brokerage accounts for other investments.

Diversify: Spread your investments across various assets to reduce risk.

Start small: Begin with small amounts and gradually increase your investments as you become more comfortable and knowledgeable.

Investing is a powerful way to build wealth over time, so starting early and staying consistent is key

8. How can I avoid overspending and impulse purchases?

Implement strategies like creating a budget, setting spending limits, and practicing mindfulness when making purchasing decisions.