Creating a budget is one of the most important steps you can take to achieve financial stability and success. A well-structured budget helps you manage your money, save for future goals, and avoid unnecessary debt. In this guide, we will walk you through a step-by-step process on how to create a budget that works for you. Whether you’re a budgeting novice or looking to refine your financial strategy, these steps will provide a solid foundation for financial well-being.

7 Steps to Create a Budget That Works for You

Creating a budget that works for you is essential for financial stability and success. By following these 7 steps, you’ll learn how to create a budget, how to track track your income and expenses, set realistic goals, and allocate your money effectively. This guide will help you take control of your finances and achieve your financial objectives.

Step 1: Determine Your Financial Goals

Before diving into the numbers, it’s essential to understand why you’re budgeting. Financial goals give purpose to your budgeting efforts and help you stay motivated. Goals can be short-term or long-term, depending on what you want to achieve.

Short-Term Goals

Short-term goals are typically achievable within a year or less. These might include:

- Building an emergency fund

- Paying off a specific debt

- Saving for a vacation or a major purchase

Long-Term Goals

Long-term goals require more time and planning. These could include:

- Saving for retirement

- Buying a home

- Funding your child’s education

Clearly defined goals will guide your budgeting decisions and help you prioritize your spending.

Step 2: Track Your Income and Expenses

To create an effective budget, you need a clear picture of your financial situation. This starts with tracking your income and expenses.

Identifying All Sources of Income

Begin by listing all sources of income, including:

- Salary or wages

- Bonuses and commissions

- Freelance work

- Investment income

- Any other sources

Knowing your total income helps you determine how much you have available to allocate towards your expenses and savings.

Categorizing Expenses

Next, categorize your expenses. Common categories include:

- Fixed expenses: Rent/mortgage, utilities, insurance

- Variable expenses: Groceries, transportation, entertainment

- Discretionary expenses: Dining out, hobbies, subscriptions

Tools and Methods for Tracking

There are various tools available to help you track your income and expenses, such as:

- Spreadsheets (Excel, Google Sheets)

- Budgeting apps (Mint, YNAB, PocketGuard)

- Manual tracking with notebooks

Choose a method that suits your lifestyle and helps you stay organized.

Step 3: Analyze Your Spending Habits

Once you have tracked your income and expenses, it’s time to analyze your spending habits. This step involves reviewing your past expenses to identify patterns and areas where you can make improvements.

Reviewing Past Expenses

Look at your spending over the past few months. Identify categories where you tend to overspend and those where you have room to cut back.

Identifying Patterns and Areas for Improvement

Are there any unnecessary expenses you can eliminate? For example, dining out frequently or subscribing to multiple streaming services may be areas to reduce spending.

Comparing Income vs. Expenses

Calculate the difference between your total income and total expenses. If you’re spending more than you earn, it’s crucial to identify areas where you can cut back to avoid going into debt.

Step 4: Set Your Budget Categories

With a clear understanding of your financial situation and spending habits, you can now set your budget categories. These categories will help you allocate your income towards necessary expenses and savings.

Essential Categories

These are non-negotiable expenses that you must cover each month, such as:

- Housing (rent/mortgage)

- Utilities (electricity, water, gas)

- Food (groceries)

- Transportation (car payments, fuel, public transport)

- Insurance (health, auto, home)

Non-Essential Categories

These expenses are not critical for your survival but contribute to your quality of life. Examples include:

- Entertainment (movies, concerts)

- Dining out

- Hobbies and leisure activities

- Personal care (haircuts, beauty treatments)

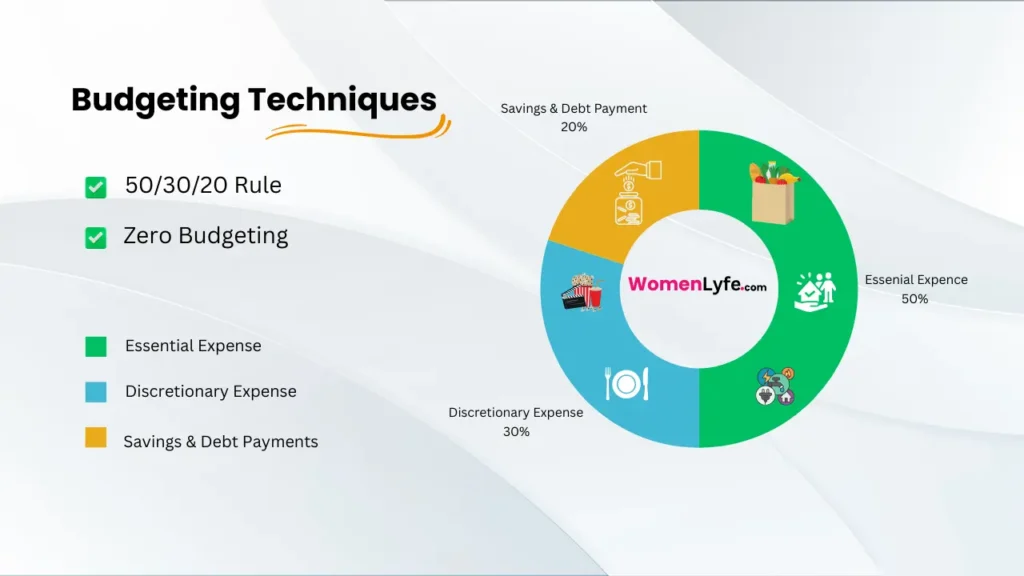

Allocating Percentages or Amounts

Decide how much of your income to allocate to each category. A common budgeting method is the 50/30/20 rule, where:

- 50% of your income goes to essential expenses

- 30% goes to discretionary expenses

- 20% goes to savings and debt repayment

Adjust these percentages based on your financial goals and priorities.

Also read

Step 5: Create Your Budget Plan

Now that you’ve set your categories and allocations, it’s time to create your budget plan. This step involves putting everything together in a structured format.

Using a Spreadsheet or Budgeting App

Choose a platform that works best for you. Spreadsheets offer flexibility and customization, while budgeting apps provide convenience and automation.

Setting Limits for Each Category

Within your chosen platform, set limits for each category based on the allocations you decided earlier. Ensure these limits align with your financial goals and income.

Prioritizing Expenses

When creating your budget, prioritize essential expenses first. Once these are covered, allocate funds to discretionary expenses and savings. This ensures your basic needs are met before spending on non-essentials.

Step 6: Implement and Stick to Your Budget

Creating a budget is just the beginning. To achieve financial success, you must implement and stick to your budget.

Tips for Staying on Track

- Regularly review your budget to ensure you’re staying within your limits.

- Use budgeting tools to track your spending in real-time.

- Set reminders for bill payments to avoid late fees.

- Keep your financial goals in mind to stay motivated.

Monitoring and Adjusting as Needed

Life is unpredictable, and your budget may need adjustments. Regularly monitor your income and expenses to identify any deviations. If your financial situation changes, be flexible and adjust your budget accordingly.

Dealing with Unexpected Expenses

Unexpected expenses can derail your budget. To handle these, build an emergency fund that covers at least three to six months of living expenses. This fund will provide a financial cushion in case of emergencies.

Step 7: Review and Adjust Your Budget Regularly

A budget is not a set-it-and-forget-it tool. Regular reviews are essential to ensure it remains effective and aligned with your goals.

Monthly or Quarterly Reviews

Schedule monthly or quarterly reviews to assess your budget’s performance. Compare your actual spending to your budgeted amounts and identify any discrepancies.

Making Adjustments Based on Changes

As your life circumstances change, so should your budget. Whether you receive a raise, incur new expenses, or achieve a financial goal, adjust your budget to reflect these changes.

Keeping Your Financial Goals in Mind

During each review, revisit your financial goals. Ensure your budget aligns with these goals and adjust as necessary to stay on track.

Conclusion

Creating and maintaining a budget is a powerful tool for achieving financial success. By following this step-by-step guide on how to create a budget, you’ll gain control over your finances, reduce stress, and work towards your financial goals. Remember, consistency and regular reviews are key to a successful budget. Stay committed, and you’ll reap the rewards of financial stability and freedom.

Frequently Asked Questions

What is a budget?

A budget is a financial plan that outlines expected income and expenses over a specific period. It helps individuals or organizations manage their money, allocate resources, and achieve financial goals by tracking spending and ensuring it aligns with their priorities and limits.

Why Is It Important to Create a Budget?

Creating a budget is important because it helps manage money effectively, ensures expenses do not exceed income, aids in saving for future goals, reduces financial stress, and provides a clear picture of spending habits, enabling better financial decisions.

Where Can You Find Resources to Create a Budget?

You can find resources to create a budget through budgeting apps (e.g., Mint, YNAB), financial websites (e.g., NerdWallet, Investopedia), books (e.g., “The Total Money Makeover” by Dave Ramsey), and financial advisors who offer personalized budgeting advice.

Who Can Help You Create a Budget?

Financial advisors, certified financial planners, and budgeting coaches can help you create a budget. Additionally, there are numerous online tools, apps, and resources available to guide you through the budgeting process.

Who Can Help You Create a Budget?

Financial advisors, certified financial planners, and budgeting coaches can help you create a budget. You can also use online tools and budgeting apps for assistance.